[ad_1]

The Indian startup ecosystem entered 2025 with caution. Venture capital funding slipped 11.03% compared to 2024, signalling that investor restraint was the mood of the market. Yet, the picture wasn’t uniformly bleak. Even as private funding slowed, startups tapping public markets surged, with IPO-bound companies raising 40% more capital than in 2024.

That contrast — between muted VC cheques and buoyant public listings — defined much of the year. And as 2026 begins, there are early signs that sentiment may be shifting again. January saw venture funding reach $927 million, a 30% increase from the same period last year, offering a shot of optimism for founders and investors.

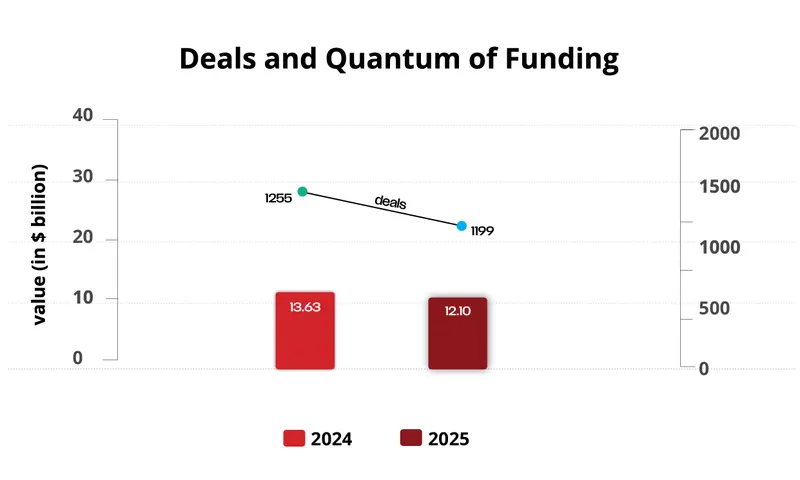

Indian startups have been experiencing quite a dramatic funding cycle over the past few years. After peaking at $44 billion in 2021, there was a sharp drop to $22.9 billion in 2022, and then a crash to $10.8 billion in 2023.

A recovery began in 2024 with investments climbing to $13.6 billion, but momentum softened in 2025 as total VC funding settled at $12.1 billion.

This in-depth funding report examines what lies beneath the headline numbers — tracking how capital was distributed across stages, which sectors attracted the most investor interest, and which sectors emerged as the gainers and losers.

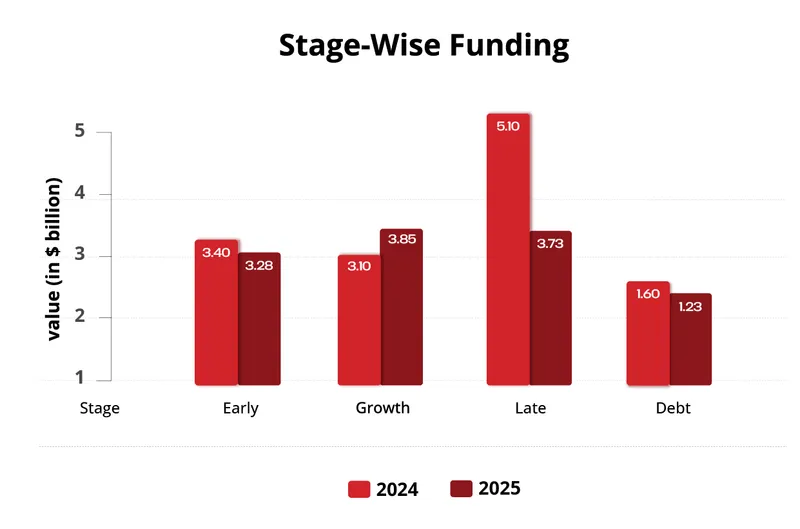

One of the more unexpected takeaways from 2025 was the near-uniform distribution of funding across stages. Early, growth, late-stage and debt funding each hovered around the $3 billion mark. The standout positive within this was the continued vibrancy of early-stage funding, which remained strong in terms of capital deployed and deal volume.

This sustained activity signals that investors are still willing to back entrepreneurs early in their journeys, betting that many of these companies will scale meaningfully in the years ahead.

Geographically, however, the picture was less encouraging. Startup and investor activity in 2025 remained heavily concentrated in familiar hubs. Bengaluru, Mumbai, and Delhi-NCR continued to dominate the ecosystem, retaining their top three positions without any change in the pecking order. The lack of movement underscores how much ground still needs to be covered before startup activity meaningfully penetrates other metros and emerging cities across the country.

The brightest spot for the Indian startup ecosystem in 2025 came from the public markets. A total of 18 startups went public during the year, raising Rs 41,284 crore — a 40% increase over 2024, when IPO-bound startups raised Rs 29,247 crore. This surge highlights growing investor confidence in new-age companies and marks a critical maturation point for the ecosystem.

Strong IPO performance is a positive signal across the board for founders seeking exits, investors looking for liquidity, and employees holding equity. Public market validation places these companies in a different orbit altogether, strengthening their credibility and opening up new avenues for long-term growth.

As mentioned earlier, January 2026 saw startup funding close to the $1 billion mark, raising hope that momentum could carry forward. That said, external macroeconomic volatility remains a key variable and will inevitably influence capital flows into the startup ecosystem.

However, optimism persists — driven largely by the resilience and adaptability of Indian startup founders. In fact, AI infrastructure startup Neysa raised $1.2 billion earlier this month, entering the unicorn club, raising hope for the industry’s potential for VC money.

That entrepreneurial grit continues to be one of the ecosystem’s strongest assets and is expected to help sustain momentum through an evolving and often unpredictable funding landscape.

For a detailed analysis and deeper insights into key trends shaping the ecosystem, download YourStory Research’s Annual Funding Report 2025.

Click here to get the full report.

[ad_2]