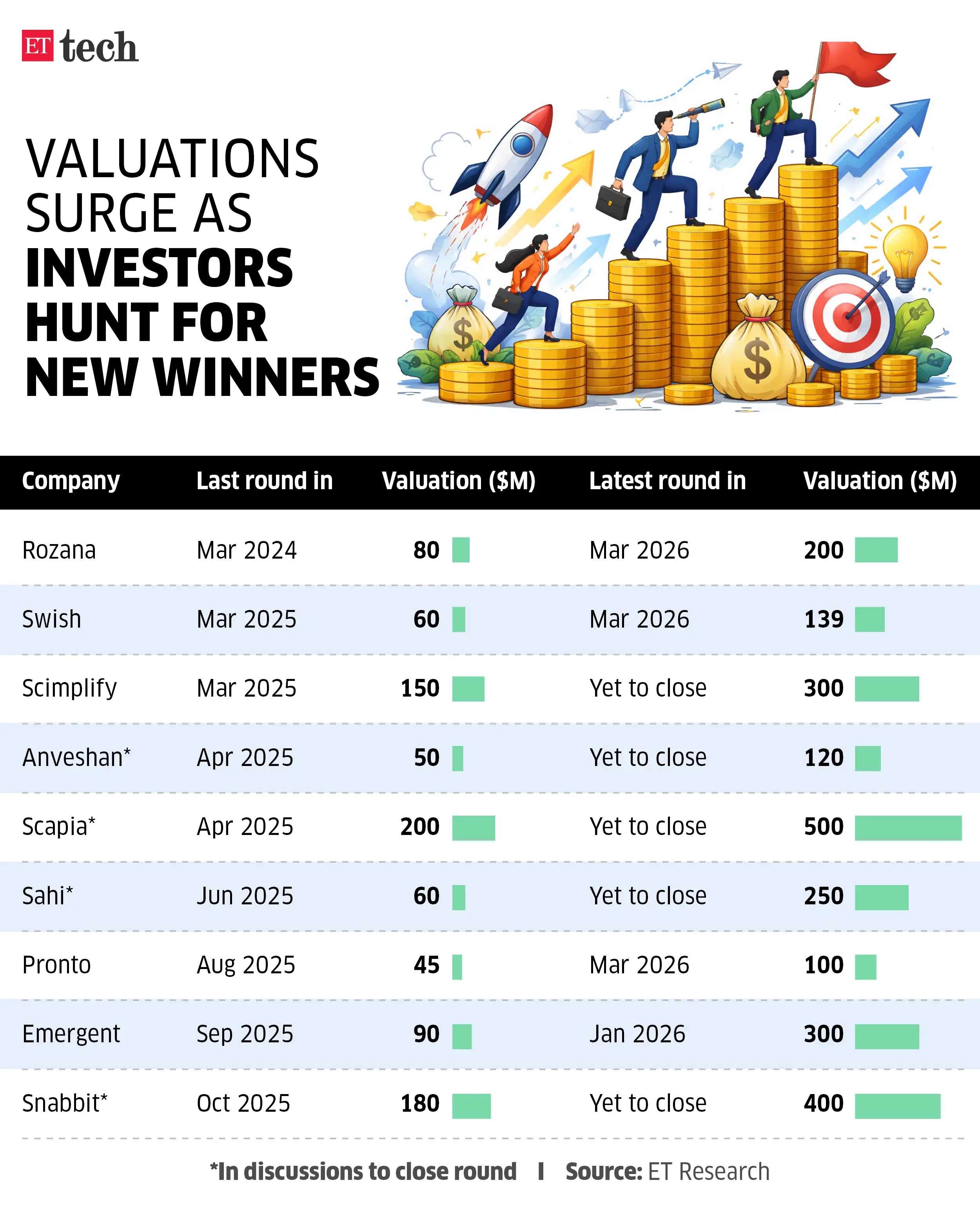

Consider these: Quick food delivery startup Swish saw its valuation more than double from around $60 million in March last year to $139 million last month. It raised the latest capital from Bain Capital Ventures, UK-based fund Hara Global and Accel.

ET reported on March 15 that Bengaluru-based travel fintech startup Scapia is negotiating a round to raise capital from General Catalyst.

People in the know said the valuation for Scapia founded by former Flipkart executive Anil Goteti is likely to see its valuation go past $500 million, more than doubling from its last previous financing last year.

Venture capitalists and investment bankers underscore that with traditional pockets of growth-stage opportunities thinning out and late-stage capital increasingly behaving like private equity, investors are narrowing their focus to a smaller set of companies that can still deliver outsized returns.

ETtech

ETtech

AI companies gain traction

While artificial intelligence startups that have hogged most of the global risk capital haven’t seen the same scale in India, a few like Sarvam AI and Emergent are finding investor interest.

Vibe-coding startup Emergent raised capital from Khosla Ventures and SoftBank in January at a $300 million valuation, more than trebling from $90 million four months prior.

Sarvam AI, which is developing large language models, is in discussions with various venture capital backers to raise its next funding round at a $1.4-1.5 billion valuation, up from its last valuation of $150-200 million in 2023. Sarvam, which is fast becoming a flagship player in India’s push for sovereign AI capabilities, is discussing a $250-300 million fundraise from global investors including Bessemer Venture Partners, chipmaker Nvidia as well as Indian IT services company HCLTech.

In the fast-growing instant house-help industry, Pronto closed a round from Epiq Capital, General Catalyst and other existing backers at a $100 million valuation last month, up from $45 million in August last year. Its rival Snabbit is also excepted to see a twofold jump in valuation within six months of its previous round as it discusses a financing led by South Korean investor Mirae Asset Venture.

“Over the past few years, most of the classic growth opportunities have largely played out,” said Kashyap Chanchani, managing director at The Rainmaker Group, a homegrown investment bank. “Investor focus has shifted more toward exits and secondaries than new entries, as only very few compelling opportunities were visible. In many established sectors, companies have already scaled and even gone public. So in this scenario the big question that emerges is where can investors still find venture-style returns.”

Broader slowdown

In the year ended March, overall funding in Indian startups fell 9% to $10.1 billion across 977 deals, compared with $11.3 billion in FY25 across 1,020 deals, according to Venture Intelligence data. The decline highlights a broader slowdown in risk capital deployment, as venture investors turn more selective, focusing on emerging themes such as AI and backing differentiated business models with the potential for outsized growth.

“Earlier, growth capital was available at almost every stage. Early on, firms like Peak XV Partners and Nexus Venture Partners would write large cheques,” said a VC investor. “At the growth stage, investors such as Iron Pillar and A91 Partners would step in, followed by late-stage players like SoftBank, Prosus and Alpha Wave Global. The late-growth market is largely dominated by private equity, while early growth continues to be led by investors with venture DNA. As a result, by the time companies reach their next funding rounds, they will need to align more closely with private equity expectations.”

Prizing growth

For companies that are scoring these valuation jumps, topline growth stood out.

Direct-to-consumer (D2C) food brand Anveshan, which is discussing a fundraise from Vertex Ventures and International Finance Corporation (IFC) at a more than twofold valuation of Rs 900-1,000 crore valuation, is backed by strong revenue growth. The Gurugram-based startup is expected to close FY26 with Rs 200-220 crore in revenue, up from about Rs 75 crore in FY25, and is currently operating at an annualised run rate of Rs 325-350 crore.

Similarly, Accel-backed specialty chemicals startup Scimplify, which is raising capital at a $300 million valuation, double that of its last round in March 2025, is currently tracking an annualised revenue run rate of around Rs 800-900 crore, against recorded revenue of Rs 200 crore in fiscal 2025.

“There are a few clear trends emerging,” said Chanchani of Rainmaker. “One is AI, where companies are seeing 3x year-on-year growth, far outpacing the typical 25-30%, making it an obvious draw for venture investors. Another is the rise of challenger companies. While early growth rounds are relatively easy to access, expectations shift at scale, with greater emphasis on profitability and defensibility.”

As a result, only a limited set of startups are able to offer returns meaningfully above typical private equity outcomes, leading to VCs doubling down on these opportunities, he said.

ET reported on April 2 that stockbroking startup Sahi is negotiating a round that could push up its valuation fourfold to around $250 million in under a year from $60 million. It’s in talks with Accel Growth Fund, Bessemer Venture Partners, Susquehanna International Group and others.

“The stockbroking space is such that investors have seen profit pools being made and therefore they know that it’s not a winner-takes-all market,” said one of the investors cited above. “If the founding team and product have quality, investors are able to build conviction. That’s what happened with Groww, which came into a market that already had Zerodha and the traditional stockbrokers but was still able to deliver what was perhaps among the largest venture outcomes for a VC in India.”