A string of recent acquisitions in India’s D2C space has underlined how lucrative these exits have been for early backers in a short span.

On February 12, USV Pharma, maker of medicines like Ecosprin, Glycomet, and Jalra, announced the purchase of a 79% stake in Wellbeing Nutrition for Rs 1,583 crore in an all-cash deal, expanding into the nutraceutical supplement and wellness space.

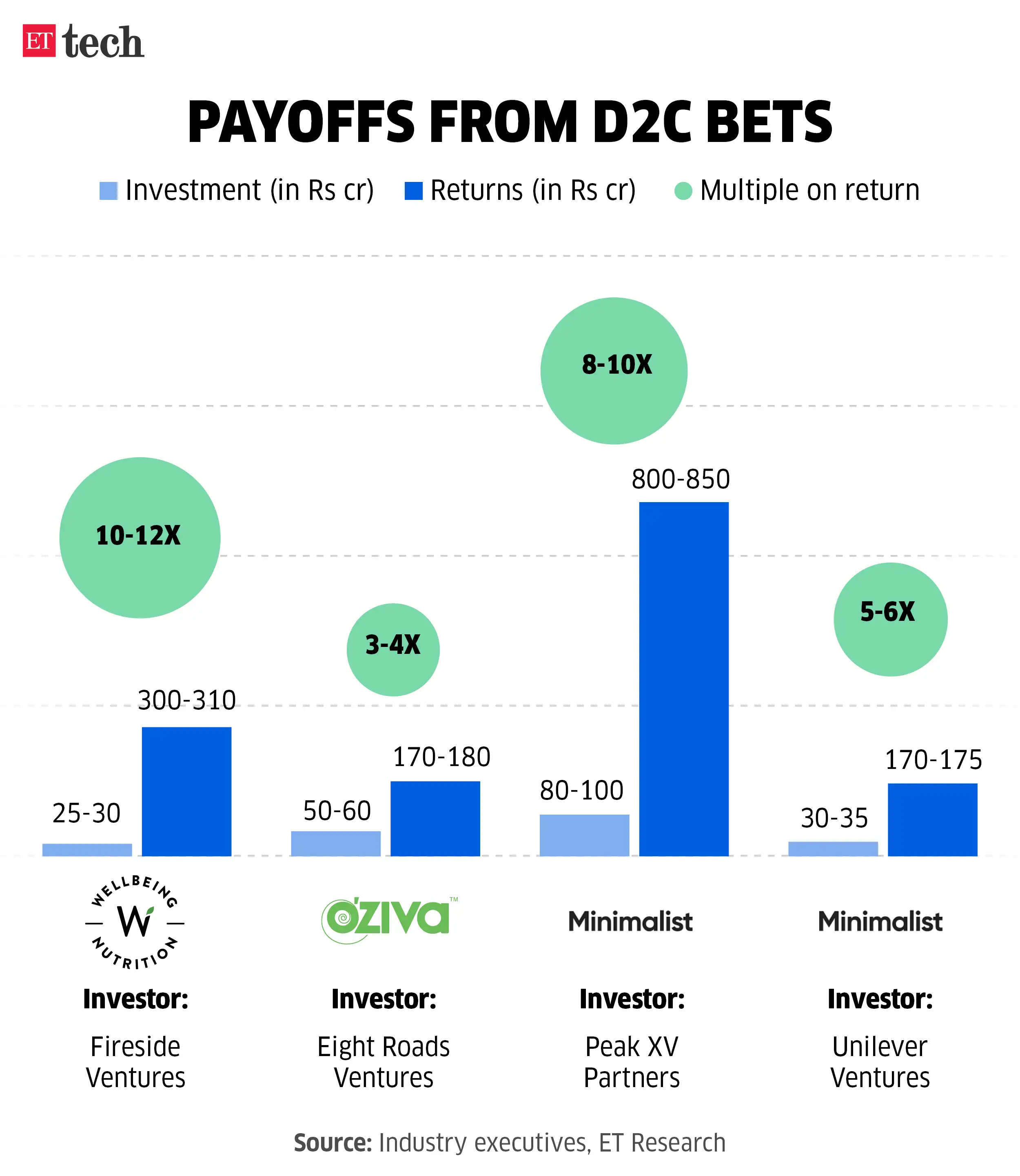

ETtech

ETtechFor Fireside Ventures, the investment in Wellbeing Nutrition was one of the key consumer bets from its Rs 863 crore second fund. The VC firm had invested about Rs 25-30 crore for about 20% stake in the Mumbai-based health and supplements brand. The stake sale yielded returns of Rs 300-310 crore, a 10-12X multiple in about four years.

Similarly, plant-based supplements brand Oziva delivered strong gains for its early backer Eight Roads Ventures. Last week, Hindustan Unilever (HUL) completed its acquisition of the brand after buying the remaining 49% stake in the company for Rs 824 crore.

Eight Roads’ Rs 50-60 crore investment against about 8% stake turned to Rs 170-180 crore, about four times its investment after HUL bought Oziva’s 51% stake in 2022.

“It’s a very good signal for the whole startup ecosystem — strategics are valuing startups well because the acquisition fits their strategy, fills a gap in their portfolio, and they believe the valuation will pay for itself,” said Kannan Sitaram, cofounder and partner at Fireside Ventures.

For VC firms, the latest deals underscore an expansion of the buyer universe beyond financial investors, improving the probability of exits, according to Sitaram.

At science-led skincare brand Minimalist, Peak XV invested about Rs 80-100 crore for a 26–28% stake in the brand in 2019. In 2024, HUL acquired Minimalist at an estimated valuation of Rs 2,670 crore. Peak XV’s stake yielded about Rs 800-850 crore, translating into a 8-10X return.

Wait and watch

To be sure, these returns look spectacular, but they are limited to the deal level. On a fund level, things could be different. Typically, in the consumer segment, VCs invest by issuing multiple small cheques to brands.

“In venture capital, you’ll end up making 20 to 25 concentrated bets of about $1–2 million. Only two to three of them will actually return capital,” said Avnish Chhabria, founder of Wellbeing Nutrition.

Take Fireside’s second fund, for instance. It was launched in 2019 with plans to invest in about 20 startups. However, not every company has delivered returns to the VC firm like Wellbeing Nutrition, Mamaearth, or Boat.

“For Fireside’s Fund 2, which we were a part of, only four have given strong returns,” said Chhabria. “So, it’s a wait-and-play game. Once you understand there’s a trade-off that a few winners will drive the fund, then you play that game.”

Old playbook

VC firms are able to make early and highly profitable exits due to the strong interest among FMCG giants to grow their portfolios through D2C acquisitions.

HUL, ITC, Marico, and Emami, are known to have either acquired or taken controlling stakes in at least a dozen digital-first brands as these FMCG firms moved to exploit the ecommerce boom.

Over the past five years, the partnerships have helped the brands significantly scale up distribution networks pan-India while leveraging the marketing muscle of the FMCG companies.

“For a D2C brand, these acquisitions act as a growth lever as they get access to FMCG’s supply chain, manufacturing scale and marketing push,” said Vibha Harish, cofounder of Cosmix, a plant-based supplement brand. Recently, Marico took a majority stake in the company.

Similarly, for an FMCG company, acquiring a well-established D2C brand offers a faster and more efficient route to enter a new category and scale it, rather than building the business from scratch, said experts.

A Crisil Ratings report noted that D2C brands grew at 40% compounded annually between fiscal 2021 and 2024, sharply outpacing legacy FMCG firms’ 9% growth. However, fewer than 15% of D2C startups crossed the Rs 250 crore revenue milestone before acquisition, and only a third were profitable.