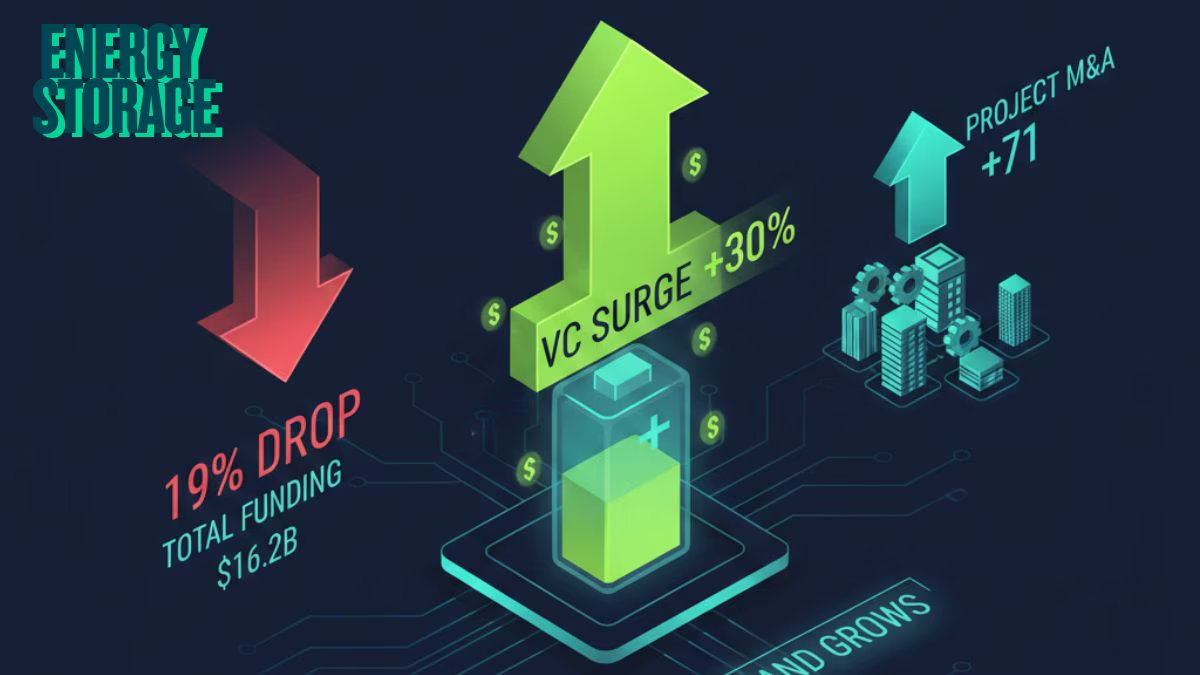

Global funding for energy storage companies cooled in 2025, falling 19% year-on-year to $16.2 billion, even as deal activity held firm and venture capital investors stepped up bets on the sector, underscoring sustained confidence in storage as a core pillar of the energy transition.

According to Mercom Capital Group’s report on global Energy Storage and Smart Grid funding and M&A activity, the sector attracted $16.2 billion across 119 deals in 2025, compared with $19.9 billion raised through 116 deals in 2024. While overall capital inflows declined, deal activity rose 3%, reflecting continued investor engagement despite a tougher policy and financing environment.

Drop in headline funding

The drop in headline funding was largely due to the absence of a few outsized debt transactions that inflated 2024 numbers, the report noted. In contrast, venture capital funding told a different story. VC investments in energy storage surged 30% year-on-year to $4.8 billion across 75 deals in 2025, up from $3.7 billion across 84 deals a year earlier.

Energy storage downstream companies emerged as the biggest VC funding recipients, followed by materials and components providers, energy storage systems companies, battery recycling firms and lithium-based battery players. The five largest VC deals in 2025 were Base Power’s $1 billion raise, KoBold Metals’ $537 million round, Group14 Technologies’ $463 million funding, green flexibility’s $411 million raise and Redwood Materials’ $350 million deal.

Debt and public market financing

Debt and public market financing for energy storage companies declined 30% year-on-year to $11.4 billion across 44 deals in 2025, compared with $16.2 billion raised in 32 deals in 2024. Despite lower capital raised, deal activity increased 38%, highlighting continued market participation.

Corporate M&A activity in energy storage moderated slightly, with 22 companies acquired in 2025 versus 25 in 2024. However, project-level M&A surged, with 65 transactions announced in 2025, marking a sharp 71% increase from 38 deals a year earlier.

The Smart Grid sector, meanwhile, recorded a strong rebound. Corporate funding rose 38% year-on-year to $3.3 billion across 84 deals in 2025, while VC funding increased 6% to $1.8 billion across 68 deals. Smart charging companies attracted the bulk of VC funding, followed by grid optimisation, distributed generation, communications and data analytics firms.

Debt and public market financing in the smart grid segment more than doubled to $1.5 billion across 16 deals, while corporate M&A activity remained broadly stable.