[ad_1]

Korea’s startup ecosystem is often described as policy-driven and well-capitalized. Annual budget announcements, multi-trillion-won venture plans, and flagship programs regularly appear in headlines. But what receives less attention is the financial plumbing underneath those announcements.

Before capital reaches a startup’s bank account, it moves through a structured institutional chain. Understanding that chain is essential for global founders, venture capital firms, and limited partners evaluating Korea’s venture capital hub within the Asia-Pacific startup ecosystem.

This discussion focuses on Korea’s funding mechanism; especially how public budget is converted into privately managed venture capital.

Where Korea’s Startup Funding Begins: Budget Allocation and Policy Capital

The venture investment policy in South Korea begins at the national budget level.

The Ministry of SMEs and Startups, known as MSS, oversees startup and venture policy. The ministry manages a multi-trillion-won annual budget, with allocations directed toward venture investment programs and contributions to the Korea Fund of Funds (see below).

However, this allocation does not immediately become startup grants. It first becomes policy capital committed into investment vehicles.

Korea does not fund startups randomly. The government allocates the budget first, then engineers that budget into structured financial instruments.

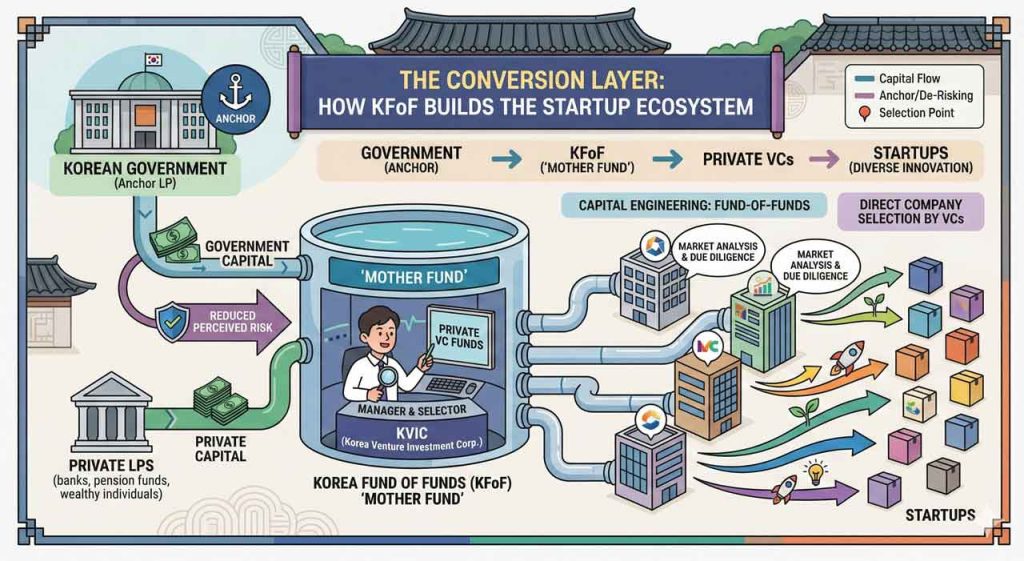

The Conversion Layer: Korea Fund of Funds and the Role of KVIC

The core vehicle in this process is the Korea Fund of Funds, often referred to as the KFoF or “Mother Fund.”

The Korea Fund of Funds operates as a government-backed fund-of-funds. Unlike general perceptions, the fund does not invest directly into startups. Instead, it commits capital into venture capital funds managed by private firms.

The Korea Venture Investment Corporation, or KVIC, manages this vehicle. KVIC selects and oversees venture fund managers that receive capital commitments.

In this structure, the government acts as an anchor limited partner. By committing capital first, it lowers perceived risk and encourages participation from private limited partners.

This is capital engineering rather than direct company selection.

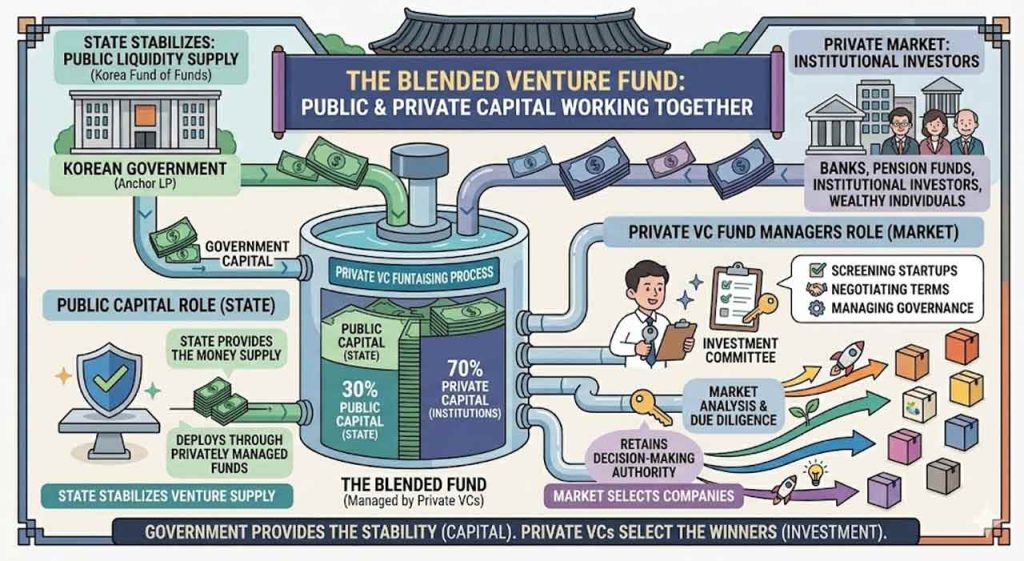

How Public Capital Blends into Private Venture Funds

Once the Korea Fund of Funds commits capital, private venture firms raise funds that include government-backed LP commitments alongside private institutional investors.

Those venture capital firms retain responsibility for screening startups, negotiating investment terms, and managing governance.

Public capital shapes liquidity conditions in the market. It does not replace private investment committees. The Fund of Funds emphasize that government capital is deployed through privately managed funds. The decision-making authority over individual startup investments remains with those fund managers.

The state stabilizes venture supply. The market selects companies.

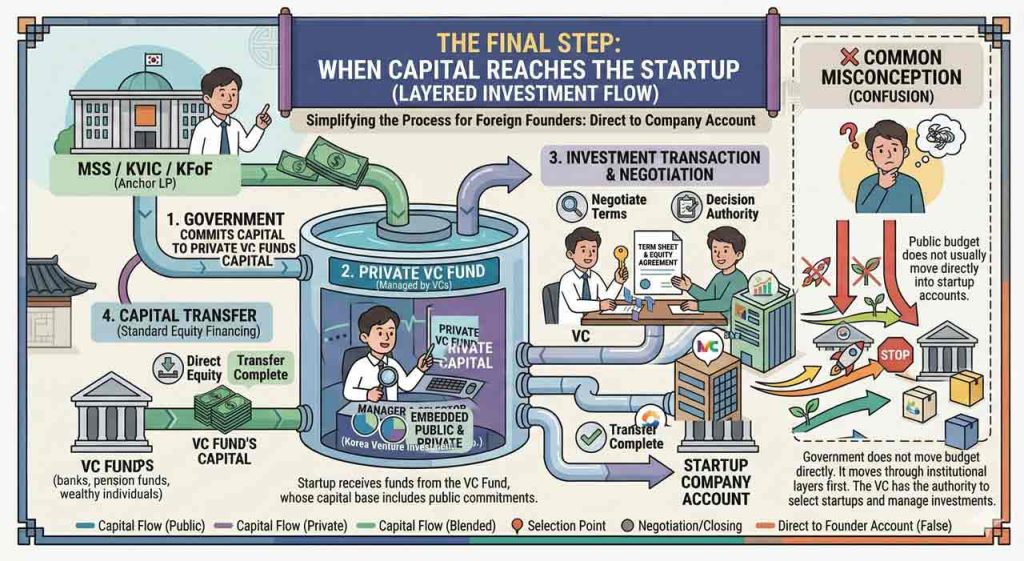

The Final Step: When Capital Reaches the Startup

When a venture fund backed by the Korea Fund of Funds invests in a startup, the transaction follows standard equity procedures.

Investment terms are negotiated between the venture firm and the startup. Once closed, capital is transferred into the company’s bank account as equity financing.

At this stage, public capital is embedded within a private round.

The startup does not typically receive funds directly from MSS or KVIC under this model. Instead, it receives investment from a venture fund whose capital base includes public commitments.

This answers a common point of confusion among foreign founders: government budget does not usually move straight into startup accounts. It moves through institutional layers first.

What This Structure Means for Global Founders and Investors

Korea’s venture capital policy is designed to reduce early-stage liquidity risk without nationalizing investment decisions.

By acting as an anchor LP through the Korea Fund of Funds, the government expands the overall pool of venture capital available in the market. That is why in recent years Korea’s government has reportedly outlined multi-trillion-won plans to mobilize venture funds through this mechanism.

For global venture firms, this signals a state-backed liquidity stabilizer.

At the same time, founders should recognize that access to public-backed capital typically depends on building relationships with locally active venture funds.

Meanwhile, institutional investors assessing cross-border venture exposure may see Korea’s model as a coordinated system where fiscal resources are channeled into market-based instruments instead of direct state ownership.

Instead of investing directly into startups, Korea relies on institutional layering to influence venture liquidity through private fund managers.

Strategic Outlook: Korea’s Venture Liquidity Model in a Shifting Capital Cycle

Across the Asia-Pacific region, governments are searching for ways to stabilize venture financing without distorting market incentives. Korea’s Fund of Funds structure reflects one such approach.

Rather than deploying capital directly into companies, the state embeds fiscal resources into privately managed vehicles. MSS allocates the budget. KVIC converts those allocations into LP commitments. Venture firms then execute investment decisions under market discipline.

This architecture changes how Korea’s venture market should be assessed. Program announcements alone do not capture the system’s depth. Liquidity conditions are shaped upstream, at the fund formation stage.

During periods of global capital tightening, anchor LP commitments can cushion fundraising slowdowns. When capital flows return, the same mechanism can accelerate fund creation.

The long-term effectiveness of this structure will hinge on fund manager selection standards, transparency in capital deployment, and the continued willingness of private LPs to participate alongside public commitments.

Key Takeaways

- Korea’s startup funding system begins with national budget allocation under the Ministry of SMEs and Startups.

- Public capital is committed into the Korea Fund of Funds, managed by Korea Venture Investment Corporation.

- The Fund of Funds invests in privately managed venture capital funds, not directly in startups.

- The government acts as an anchor limited partner to attract private LP capital.

- Venture firms retain independent authority over startup selection and investment terms.

- Startups receive equity capital through private venture rounds that include public-backed LP commitments.

- The structure reduces liquidity risk while maintaining market-based decision-making.

- For global founders and investors, access to public-backed capital typically depends on engagement with local venture funds integrated into Korea’s policy framework.

🤝 Looking to connect with verified Korean companies building globally?

Explore curated company profiles and request direct introductions through beSUCCESS Connect.

– Stay Ahead in Korea’s Startup Scene –

Get real-time insights, funding updates, and policy shifts shaping Korea’s innovation ecosystem.

➡️ Follow KoreaTechDesk on LinkedIn, X (Twitter), Threads, Bluesky, Telegram, Facebook, and WhatsApp Channel.

[ad_2]