[ad_1]

Valuation Metrics: A Closer Look

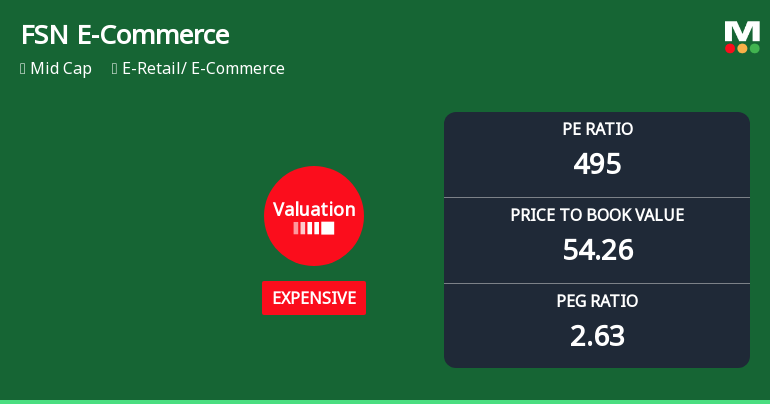

At present, FSN E-Commerce Ventures trades at a P/E ratio of 495.16, a figure that remains exceptionally high but has moderated enough to prompt a downgrade in its valuation grade from very expensive to expensive. This adjustment reflects a subtle easing in market expectations or earnings growth assumptions, yet the stock remains priced at a significant premium compared to its sector peers.

The company’s price-to-book value stands at 54.26, underscoring the market’s willingness to pay a substantial premium over the book value of its assets. This elevated P/BV ratio is indicative of investor confidence in FSN’s growth prospects and intangible assets, such as brand value and technological infrastructure, which are critical in the e-commerce space.

Other valuation multiples further illustrate the premium valuation: the enterprise value to EBIT ratio is 216.24, and the EV to EBITDA ratio is 115.42. These multiples are considerably higher than typical industry averages, signalling that investors are pricing in robust future earnings growth despite current profitability metrics.

Comparative Analysis with Sector Peers

When benchmarked against notable FMCG and consumer goods companies such as Marico, Dabur India, and Colgate-Palmolive, FSN’s valuation multiples stand out. Marico, for instance, is rated very expensive with a P/E of 61.57 and an EV to EBITDA of 46.1, while Dabur India’s P/E is 49.35 and EV to EBITDA 36.68. Colgate-Palmolive also carries a very expensive tag with a P/E of 45.53 and EV to EBITDA of 31.98.

These comparisons highlight FSN’s valuation as an outlier, reflecting the market’s elevated growth expectations for the e-commerce sector relative to traditional consumer staples. However, the PEG ratio of 2.63 for FSN, while higher than some peers, suggests that the stock’s price is somewhat justified by its expected earnings growth, albeit at a premium.

Financial Performance and Returns

FSN’s return on capital employed (ROCE) is 10.69%, and return on equity (ROE) is 7.55%, figures that are modest given the valuation multiples. These returns indicate that while the company is generating positive returns on invested capital, the profitability metrics have yet to fully catch up with the market’s lofty valuation.

From a price performance perspective, FSN has delivered impressive returns over the medium term. The stock has appreciated by 61.15% over the past year and 84.95% over three years, significantly outperforming the Sensex, which returned 10.44% and 38.28% over the same periods respectively. This outperformance underscores investor enthusiasm for FSN’s growth trajectory despite recent short-term volatility.

In the short term, however, the stock has seen a 1.39% decline on the latest trading day, closing at ₹263.00 against a previous close of ₹266.70. The 52-week trading range of ₹154.90 to ₹285.60 reflects considerable price volatility, typical of high-growth e-commerce stocks.

Mojo Score and Rating Upgrade

Reflecting the evolving valuation and fundamentals, FSN E-Commerce Ventures’ Mojo Score currently stands at 70.0, with a Mojo Grade upgraded to Buy from Hold as of 24 February 2026. This upgrade signals increased confidence in the stock’s medium-term prospects, supported by its strong market position in the e-retail sector and improving financial metrics.

The company’s market capitalisation grade remains at 2, indicating a mid-cap status that balances growth potential with manageable risk. The rating upgrade is a significant endorsement for investors seeking exposure to the burgeoning e-commerce industry, which continues to benefit from structural shifts in consumer behaviour and digital adoption.

Sector and Market Context

The e-retail sector remains one of the fastest-growing segments in India’s economy, driven by rising internet penetration, increasing smartphone usage, and evolving consumer preferences. FSN E-Commerce Ventures, as a key player in this space, is well-positioned to capitalise on these trends, although the sector’s competitive intensity and regulatory environment pose ongoing challenges.

Comparatively, traditional consumer goods companies, while exhibiting stable earnings and dividends, have more modest growth prospects. This divergence explains the premium valuations commanded by FSN despite its relatively lower profitability ratios.

Investors should weigh the company’s high valuation multiples against its growth potential and market leadership. The current price correction and valuation grade shift may offer a more attractive entry point for long-term investors willing to tolerate short-term volatility.

Investor Takeaway

FSN E-Commerce Ventures Ltd’s valuation adjustment from very expensive to expensive reflects a nuanced shift in market sentiment. While the stock remains richly valued, the moderation in multiples combined with a recent rating upgrade suggests improving price attractiveness for discerning investors.

Given the company’s strong growth record, sector tailwinds, and upgraded Mojo Grade, FSN presents a compelling case for inclusion in growth-oriented portfolios. However, investors should remain mindful of the elevated valuation risks and monitor quarterly earnings and sector developments closely.

In summary, FSN’s current valuation landscape offers a balanced view: premium pricing justified by growth potential but tempered by profitability metrics and market volatility. This dynamic underscores the importance of a disciplined investment approach when considering FSN E-Commerce Ventures Ltd as part of a diversified equity portfolio.

Only Rs. 9,999 – Get MojoOne for 1 Year + 3 Months FREE (60% Off) Start Today

[ad_2]